RRP Semiconductor doesn’t make chips. So why did the stock explode?

#020 A tiny float, a big story, and a 55,000% stock that outran its business.

TLDR:

RRP Semiconductor’s stock rose over 55,000% in under two years, despite the company having no chip manufacturing, negative revenue, and just two employees.

The rally was driven by a name change, a hot semiconductor narrative, and confusion with a separate private company owned by the same promoter.

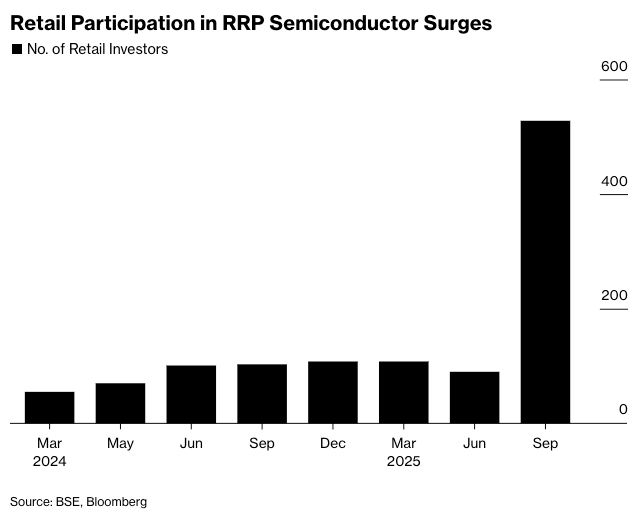

With nearly all shares locked in, only about 2% were available to trade, pushing the stock into 149 consecutive upper circuits.

Regulators eventually intervened, placing the stock under surveillance and restricting trading to once a week.

The episode is a reminder that market stories and scarcity can overpower fundamentals, at least temporarily.

The Bite:

In early 2024, RRP Semiconductor was a little-known stock changing hands in the ₹15–₹20 range, attracting barely any attention in the market. Less than two years later, the same share trades above ₹11,000. The move represents a rise of over 55,000%, placing the company among the most extreme stock price surges seen in recent market history.

Naturally, the internet lost its mind.

WhatsApp groups lit up. Telegram channels turned euphoric. Screenshots of portfolios were passed around like proof of divine intervention. RRP Semiconductor was suddenly everywhere, hailed as India’s answer to the global AI and chipmaking boom. A tiny company, riding a big theme, delivering life-changing returns.

But there was an uncomfortable detail lurking behind the numbers.

RRP Semiconductor didn’t actually make semiconductors.

As of its latest disclosures, the company has two full-time employees, has not started chip manufacturing, and has officially told stock exchanges that it hasn’t applied for any government semiconductor incentive schemes. In fact, its most recent financials showed negative revenue. Yet at its peak, the market valued it at more than ₹15,000 crore.

So how did a company with barely any operations become one of the world’s best-performing stocks?

To understand that, you have to look beyond balance sheets and focus on something Indian markets understand very well: scarcity, storytelling, and timing.

India is in the middle of a semiconductor obsession. The government has announced a ₹76,000 crore incentive program. Global giants like Micron, Tata Group, Foxconn, and HCL have lined up investments.

The narrative is clear: India wants to build chips, and investors want in.

The problem is, there aren’t many listed Indian companies that actually give retail investors exposure to this theme. When a powerful story meets limited investable options, markets tend to stretch logic. RRP Semiconductor walked straight into that gap.

Until early 2024, the company wasn’t even called RRP Semiconductor. It was G D Trading and Agencies Ltd, a low-profile firm with no connection to cutting-edge technology. That changed when Rajendra Chodankar entered the picture.

Chodankar, an entrepreneur whose earlier ventures included niche products like thermal imaging systems and defence-related camera equipment, took control of the listed company by settling an outstanding loan of about ₹8 crore that the original promoters owed. Instead of receiving cash, he was issued equity.

Soon after, on 23th April, the board approved a preferential allotment of shares to Chodankar and a few others at ₹12 per share, even though the stock was already trading much higher in the market. That single decision dramatically altered the company’s ownership structure.

Chodankar emerged with roughly three-quarters of the company, while the original founders were diluted to a stake of less than 2%.

Control had decisively shifted.

Around the same time, the company agreed to rename itself RRP Semiconductor Ltd. On paper, it was a procedural change. In reality, it was a narrative upgrade perfectly timed for an AI-obsessed market.

What made the story even more compelling was something that happened slightly earlier, but outside the listed company altogether. About two months before the takeover, Chodankar had incorporated a private company called RRP Electronics Pvt. Ltd. This new entity announced plans to build an outsourced semiconductor assembly and testing facility in Maharashtra.

Legally, the listed company and the private company were separate. The listed firm did not own any stake in RRP Electronics. But both were owned by the same promoter, shared similar branding, and operated under the broader RRP umbrella. For many retail investors, that distinction didn’t register.

In exchange filings, RRP Semiconductor lists RRP Electronics as a related party because of the common ownership. But “related” doesn’t mean “owned.” Any progress made by the private company does not automatically translate into assets, revenue, or business for the listed one. Still, in a euphoric market, association often gets mistaken for entitlement.

Public events added more colour to the narrative. In September 2024, RRP Electronics held an event in Navi Mumbai linked to its new unit. Chodankar spoke confidently about India’s technological future, declaring that the country was on track to become a global powerhouse. Videos from the event showed senior political leaders and even cricketing icons in attendance.

None of this changed the fundamentals of the listed company. But optics matter.

By this point, another critical factor had quietly come into play: the float.

When interest rose, there simply weren’t enough shares to go around. Every new buyer had to bid higher. If you add daily circuit limits to the mix, and prices didn’t just rise; they got mechanically pushed upward.

RRP Semiconductor hit the upper circuit 149 sessions in a row.

This wasn’t organic price discovery. It was a feedback loop. Rising prices attracted attention. Attention attracted buyers. Limited supply pushed prices higher. And higher prices reinforced the belief that something extraordinary was happening.

Financial reality barely mattered.

In the September quarter, RRP reported negative revenue after reversing sales from a large order that was later cancelled due to contractual disputes. It posted losses. It confirmed it hadn’t started semiconductor manufacturing. The company even issued clarifications saying its financials did not justify the stock price.

The market shrugged.

Eventually, regulators could no longer ignore what was happening. In October 2025, the BSE flagged unusual price movements and placed the stock under enhanced surveillance, tightening circuit filters. When that didn’t cool things down, the exchange imposed stricter measures on November 7, 2025, restricting the stock to trading once a week.

SEBI also began examining the price surge for potential wrongdoing. Past regulatory issues resurfaced, including links to promoter groups associated with a company that had been delisted years earlier and barred from accessing capital markets. Even the exchange later acknowledged there may have been internal lapses in how certain approvals were processed.

By then, the rally had finally started to wobble. The stock slipped about 6% from its peak. Not a crash, but enough to remind investors that gravity still exists.

And then came perhaps the most surreal moment of all.

The company itself wrote to the exchange asking regulators to consider resetting the stock price closer to ₹20, arguing that the existing price was artificial and disconnected from fundamentals. In other words, after a 900-fold rise, the company effectively said the stock had gone too far.

That single letter sums up the entire episode.

If RRP’s story feels oddly familiar, that’s because markets have fallen for this trick many times before. In 2017, at the peak of the Bitcoin craze, a struggling US beverage company called Long Island Iced Tea simply changed its name to Long Blockchain. Nothing else changed. No product. No tech. Yet the stock jumped nearly 300% in a single day. Regulators eventually stepped in, and the company was later thrown off the Nasdaq, becoming a global cautionary tale of buzzword investing.

India-linked markets saw something similar the same year. Longfin Corp, listed in the US but promoted by an India-born entrepreneur, saw its stock shoot up more than 2,600% in a week after announcing the acquisition of Ziddu.com, a so-called blockchain lending platform. The story sounded futuristic, the free float was tiny, and the price went vertical. It didn’t last. Investigations followed, trading was halted, and the stock crashed.

Go back further to the dot-com boom of the late 1990s and the pattern becomes even clearer. Companies would slap “.com” onto their names, talk up an internet pivot, and watch their valuations double overnight. One academic study from that period even found that name changes alone led to sharp price gains, regardless of whether the business actually changed.

Indian markets have played this game too. In past bull runs, especially around 2007 and 2014, small-cap stocks with very few tradable shares were pushed into endless upper circuits by hot themes like Smart Cities or Digital India. Many had hardly any revenue, a handful of employees, and no real execution but for a while, they were the only listed proxies investors could buy.

Seen in that light, RRP Semiconductor isn’t an outlier. It’s the latest reminder that in markets, stories travel faster than balance sheets.

RRP Semiconductor didn’t soar because it built world-class chips or cracked advanced manufacturing. It soared because it cracked market psychology. It sat at the intersection of a hot global theme, limited domestic options, a tiny trading float, social media amplification, and delayed regulatory intervention.

This doesn’t make the episode unique. Indian markets have seen similar stories before. What makes RRP different is the sheer scale and speed at which belief replaced fundamentals.

For regulators, the case exposes how difficult it is to manage speculative excess in an era where narratives travel faster than disclosures. For investors, it’s a reminder that when price movements depend more on scarcity and storytelling than on cash flows, exits can become theoretical.

RRP Semiconductor may or may not build something meaningful in the future. India may well succeed in its semiconductor ambitions. But none of that changes the lesson staring everyone in the face today.

In markets, belief can take prices very far.

But when belief breaks, reality collects interest.

Your Sunday watch

If you’re looking to watch something a little more grounded, we recently explored a very different side of India’s growth narrative. One that doesn’t play out on stock charts or trading apps, but inside warehouses where the real pressure of modern commerce shows up.

The Filter Coffee team went on-ground to understand how India’s delivery machine actually works, and what it takes to keep parcels moving at scale. That led us to a conversation with Pramod Ghadge, Co-founder and CEO of Unbox Robotics, about automation, bottlenecks, and why logistics may be one of the most under-appreciated pieces of the economy.

If that sounds like your kind of insight, the full conversation is worth a watch.

If you’ve made it this far, thanks for reading. We’ll be back next week, like clockwork.

Got a company, sector, or story you think we should dig into? Hit reply and tell us.

If we pick your suggestion, we’ll send some Filter Coffee merch your way.

Coffee Crew out.

The Long Island Iced Tea parallel was a good one. That reset was a weird occurrence. I mean, if we consider belief outrunning the balance sheets, perhaps not as bad.

The comparision to Long Island Iced Tea's blockchain pivot is spot on. I've seen this pattern play out in several market cycles and the mechanics are always similar: hot narrative, scarce float, and social media amplification. What's particularly intresting here is how the feedback loop between upper circuits and investor psychology created a self-reinforcing momentum that became completely detached from any buisness reality. The fact that the company itself asked regulators to reset the price is honestly wild.