Why are quick-commerce apps ditching 10-minute delivery?

#024 India’s quick commerce model is shifting away from the 10-minute promise as labour pressure, regulation, and profitability concerns reshape how instant delivery actually works.

TLDR:

Quick commerce in India did not end in 2026. What ended was the aggressive marketing of “10-minute delivery” after government intervention flagged safety risks and rider pressure.

The ten-minute promise mattered more psychologically than operationally, pushing impulsive buying but also creating unsafe expectations for delivery partners.

Platforms quietly shifted focus from speed alone to reliability, assortment, and higher-value categories like electronics, medicines, and personal care.

India’s quick commerce model survived where Western markets failed due to dense cities, habitual top-up buying, and lower last-mile costs.

The future of quick commerce will depend less on how fast orders arrive and more on sustainable economics, strong infrastructure, and better treatment of gig workers.

The Bite:

Between 2020 and 2026, global retail went through a sharp reset. What began as a pandemic-era convenience layer slowly turned into a race that prioritised speed above almost everything else. Groceries in ten minutes. Medicines delivered before anxiety could set in. Phone chargers arriving before batteries died.

This phase came to be known as quick commerce, or q-commerce, and it was often described as the third generation of retail. The first generation relied on centralised warehouses that delivered in days. The second shifted inventory closer through regional fulfilment hubs, compressing timelines to one or two days. The third took that logic to its extreme by placing inventory inside neighbourhoods themselves, using hyperlocal dark stores to promise delivery in minutes rather than hours.

For a while, this seemed like the inevitable destination of e-commerce. If technology allowed essentials to reach homes in ten minutes, why should anything take longer.

But by January 2026, the experiment hit a clear inflection point. Regulatory intervention, worker unrest, and a visible change in how investors viewed the sector forced platforms to step back from rigid time guarantees. The industry did not walk away from speed. It walked away from loudly advertising speed as a non-negotiable promise.

To understand why this moment mattered, it helps to understand how the ten-minute delivery promise became so powerful in the first place.

The desire for faster delivery is not new. Long before smartphones and apps, companies tried to compress delivery timelines. In the late 1990s, startups like Kozmo.com in the United States promised one-hour delivery for everyday goods. The idea failed spectacularly, not because consumers did not value speed, but because the infrastructure required to make it viable did not exist. There was no real-time GPS tracking, no predictive demand modelling, and no dense network of small warehouses embedded within cities.

Two decades later, those constraints disappeared. By the late 2010s, smartphones were ubiquitous, mapping had become precise, and logistics software could optimise routes dynamically. Around 2019, several companies began experimenting with local fulfilment centres designed to serve small neighbourhood clusters rather than entire cities. Delivery times dropped below thirty minutes. Costs were high, but the model was finally feasible.

Then Covid arrived and rewired consumer behaviour almost overnight.

Lockdowns in early 2020 shut physical stores and pushed households online for essentials. Online grocery demand surged globally, with some estimates pointing to an 80% increase in purchases in a single year. In India, ordering groceries online stopped being a convenience feature and became a practical necessity.

What mattered more than the initial spike was what followed. Even after restrictions eased, consumers did not fully revert to old habits. Weekly planned grocery trips gave way to frequent, smaller top-up purchases. Milk ran out unexpectedly. Bread was needed late in the evening. Snacks were ordered impulsively. These were not large, price-sensitive baskets. They were urgency-driven decisions.

Quick commerce fit perfectly into this gap.

Platforms realised that the real opportunity was not in delivering full grocery carts faster, but in owning the moments when people did not want to think ahead. If an app could reliably deliver within fifteen minutes, it could become the default solution for everyday friction.

This is where dark stores became central to the model.

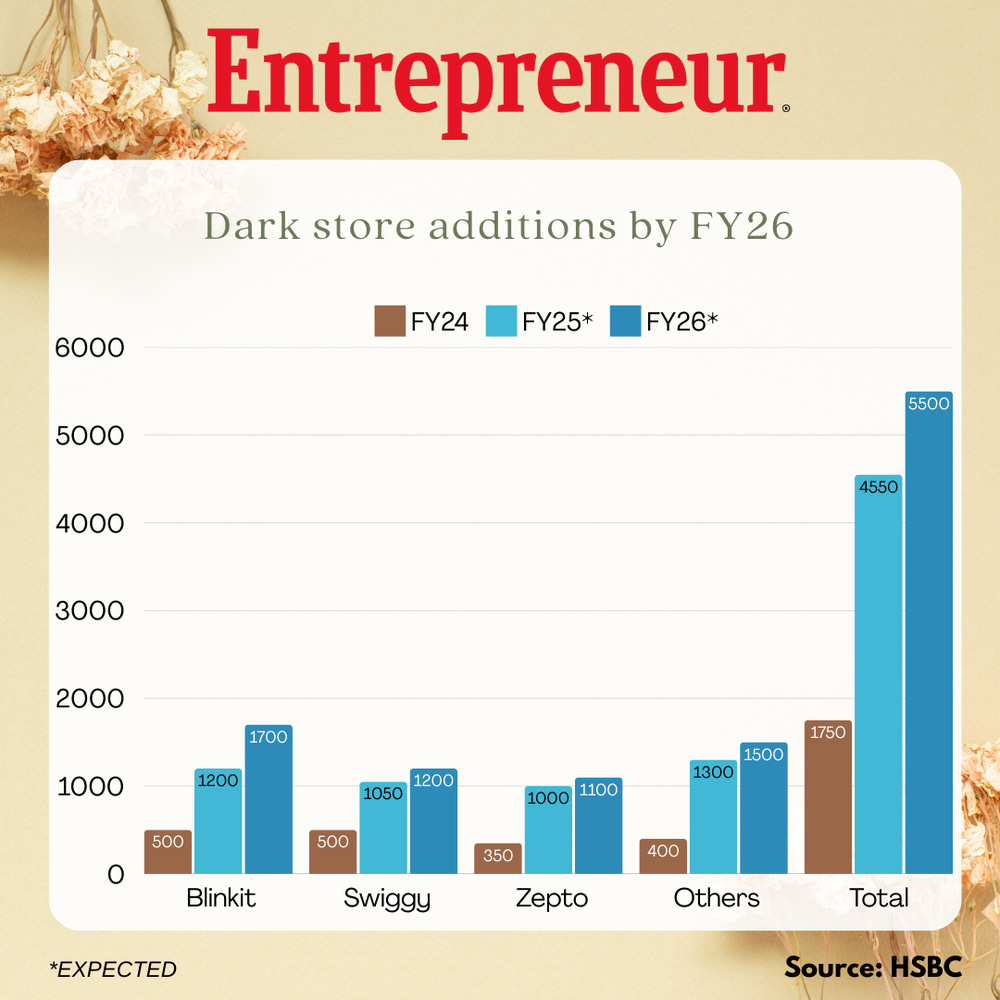

Dark stores were compact warehouses placed inside residential areas, closed to walk-in customers and optimised entirely for speed. A traditional supermarket carries anywhere between 15,000 and 60,000 stock-keeping units. A dark store typically carries 2,000 to 3,000 high-velocity items. These are products that sell daily and turn over quickly.

The economics were simple. Shorter distances meant lower delivery times. Smaller assortments meant faster picking. Delivery radii could be kept under two or three kilometres. Picking times could be compressed to under two minutes. When done well, this allowed deliveries within ten to twenty minutes without relying on reckless riding.

By 2021, several Indian players had embraced this model aggressively. Grofers was acquired by Zomato, rebranded as Blinkit, and repositioned its business around speed as a core differentiator. Zepto built its entire brand around the ten-minute promise. Swiggy Instamart scaled using Swiggy’s existing logistics network.

Speed became the headline because it was easy to communicate. Ten minutes was concrete. It was visible. It created a sense of certainty that vague claims like “fast delivery” could not.

By 2024, quick commerce in India was no longer experimental. Estimates from Business Standard and Redseer placed gross merchandise value between five and six billion dollars, with annual growth rates exceeding 75%. Some projections suggested the market could reach ₹1.5 to ₹1.7 lakh crore by 2027.

Blinkit crossed 1,000 dark stores and announced plans to expand rapidly. Zepto raised large funding rounds and expanded into electronics, beauty products, and even precious metals. Swiggy Instamart reported improving contribution margins and rising order density per store.

Front end, this model appeared to be working.

But beneath the growth numbers, pressure was building.

The ten-minute promise, while operationally achievable in dense neighbourhoods, created a psychological dynamic that was difficult to contain. Customers saw countdown timers on their screens. Delays, even when minor, triggered dissatisfaction. Ratings, complaints, and order allocations increasingly revolved around perceived speed.

Delivery partners were paid per order. Earnings depended on volume and completion time. Incentive structures rewarded faster fulfilment. Even if riders were not explicitly told to deliver within ten minutes, the system made the priority clear.

By late 2025, rider frustration spilled into public view.

Gig worker unions organised nationwide strikes on December 25 and December 31, two of the busiest days of the year for quick commerce platforms. Riders spoke openly about overspeeding, jumping traffic signals, answering customer calls while riding, and fearing penalties for delays caused by traffic, weather, or store congestion.

This time, the protests did not fade quietly.

The Union Labour and Employment Ministry intervened directly and urged platforms such as Blinkit, Zepto, and Swiggy Instamart to remove ten-minute delivery branding. Because they were more of the marketing hooks than operational realities.

Delivery times can be dynamic, influenced by distance and traffic, order volume, and store density.

Following which, last week, Blinkit removed the ten-minute delivery claim from its app and marketing. Instead, it began displaying the distance to the nearest dark store, subtly reframing delivery speed as a function of proximity rather than a guaranteed deadline. Eternal, the parent company of Zomato and Blinkit, clarified to exchanges that this change does not alter the underlying business model.

What changed was the framing but the behavioural impact of the ten-minute promise was never cosmetic.

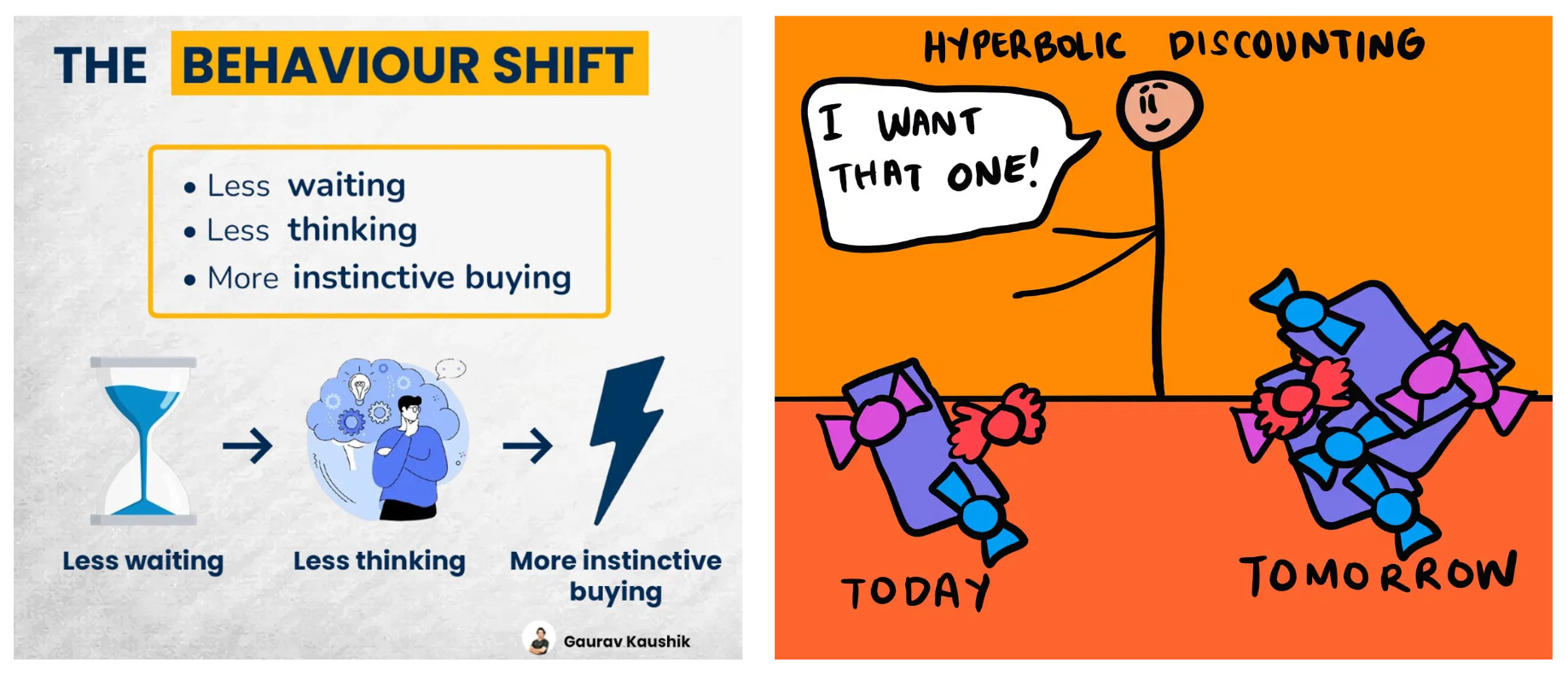

Behavioural economics explains this through hyperbolic discounting. Humans disproportionately value immediacy. When an app promises delivery in ten minutes, it short-circuits rational decision-making. Price comparisons fade. Alternatives lose relevance. Speed becomes the dominant factor.

This is why the ten-minute promise was such a powerful growth lever. It did not just compress delivery timelines. It reshaped consumer behaviour.

However, data collected after the January 2026 intervention revealed a quieter truth. Most consumers were not emotionally attached to ten minutes itself. Surveys showed that 74% of users supported removing the rigid timeline. While 100% considered ultra-fast delivery essential for medicines, only about 55% felt the same for groceries.

Nearly 40% stated they did not want anything within ten minutes at all.

The ten-minute promise, it turned out, was more marketing escalation than fundamental consumer demand.

From a business perspective, the timing of this regulatory push aligned with deeper structural changes already underway.

Quick commerce economics had been evolving well before January 2026. Platforms increasingly recognised that groceries alone could not deliver profitability. Average order values needed to rise. High-margin categories needed to expand. Advertising and brand partnerships needed to scale.

In 2025, dark stores were becoming larger and more sophisticated. So-called megapods stocked tens of thousands of SKUs, allowing platforms to deliver electronics, appliances, and lifestyle products alongside groceries.

By 2026, non-grocery categories accounted for roughly 15–20% of GMV. It means out of every ₹100 worth of orders placed on quick commerce apps, about ₹15 to ₹20 came from items that were not groceries.

Zepto delivered iPhones within minutes of launch. Blinkit sold gold and silver coins during Dhanteras. Fashion brands experimented with one-hour delivery for impulse purchases. Pharmacy and healthcare became critical growth engines where speed genuinely mattered.

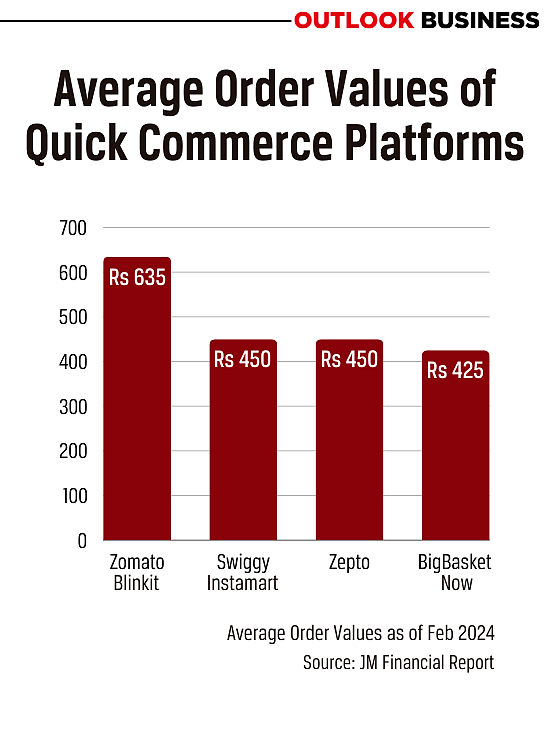

Average order values increased from ₹300–₹400 to ₹500–₹700. Swiggy Instamart reported contribution margins improving toward break-even levels. Advertising emerged as a meaningful revenue stream, with over 1,500 FMCG brands paying for sponsored placements and search visibility. Advertising contributed roughly 15% of total revenue and carried significantly higher margins than delivery fees.

The business no longer needed speed to do all the heavy lifting.

The filing of Zepto’s confidential draft red herring prospectus with SEBI in December 2025 reinforced this shift. With public markets came scrutiny. Growth narratives had to withstand questions around cash burn and sustainability. Despite rapid revenue growth, Zepto’s FY25 losses were estimated at over ₹3,300 crore, with loss per rupee of sales increasing rather than shrinking.

Scale alone was no longer the answer.

Globally, this moment marked a clear divergence. In the United States and Europe, quick commerce collapsed between 2022 and 2024. High labour costs, lower urban density, and post-pandemic demand correction made the model unviable. Startups such as Jokr, Gorillas, Buyk, and Fridge No More shut down. Getir exited multiple countries after burning hundreds of millions of dollars.

India survived because its structural conditions were different. Dense cities, lower last-mile costs, and entrenched top-up buying habits supported the model. But the human cost of sustaining speed could no longer be ignored.

January 2026 therefore did not mark the end of quick commerce. It marked its maturation.

Looking ahead, quick commerce is increasingly merging with mainstream e-commerce. Delivery in days already feels outdated. Amazon and Flipkart have launched their own instant delivery arms. Speed is no longer a premium feature. It is a baseline expectation.

The next phase will be shaped by three forces.

Category depth will matter more than raw speed. Groceries alone will not sustain profitability. Electronics, fashion, and healthcare will.

Infrastructure will become the true moat. Dense networks of dark stores and megapods, supported by predictive logistics, will be difficult to replicate.

And the social contract will determine long-term viability. Platforms that invest in rider safety, insurance, and income stability will face lower regulatory risk and earn greater consumer trust.

The ten-minute delivery era did come to an end because unchecked speed created risks that outweighed its marketing value.

By stepping away from the stopwatch, quick commerce has finally decided to grow up.

If you’ve made it this far, thanks for reading. We’ll be back next week, like clockwork.

Got a company, sector, or story you think we should dig into? Hit reply and tell us.

If we pick your suggestion, we’ll send some Filter Coffee merch your way.

Coffee Crew out.