Why does everyone in India suddenly want a Swiss watch?

#025 India’s luxury watch boom is being driven by rising wealth, shrinking price gaps, and a new generation that treats Swiss timepieces as identity and assets.

TLDR:

India’s obsession with Swiss watches has shifted from occasional overseas purchases to everyday domestic buying, driven by faster growth in imports, easing price gaps, and a new generation that tracks, understands, and plans luxury watch purchases with intent.

Even as Swiss watch exports slowed across Asia due to weak demand in China, India emerged as one of the fastest-growing markets, with exports rising sharply and luxury watches now accounting for about 70% of the Indian watch market by value.

Rising wealth, younger high earners, and changing psychology have turned watches into visible, portable wealth, with scarcity, long waitlists, and strong resale values making brands like Rolex and Patek Philippe feel closer to assets than accessories.

A maturing pre-owned market, growing comfort with resale, and tighter supply have reinforced this shift, signalling that luxury watches in India are no longer impulse gifts but considered, long-term purchases tied to identity and value.

The Bite:

A few years ago, if someone in India bought a Rolex, it usually meant one of three things. They were getting married. They had just sold a business. Or they were flying back from Dubai and wanted to “save on duty”.

You don’t need to ask. The context was baked in.

However, today, people are buying Rolex, Cartier, Omega, Rado, Audemars Piguet, and Patek Philippe watches right here in India. They’re buying them from Indian boutiques, servicing them at Indian service centres, reselling them through Indian platforms, and then spending an unhealthy amount of time debating dial colours, case sizes, and waitlists on WhatsApp groups, Reddit threads, and Instagram comment sections.

Access is only part of the shift. Swiss watches have stopped being occasional trophies and turned into objects of daily fascination. People track releases, memorise reference numbers, know which models are impossible to get, and which ones quietly hold value.

To understand how real this shift is, it helps to look at what’s actually coming into the country.

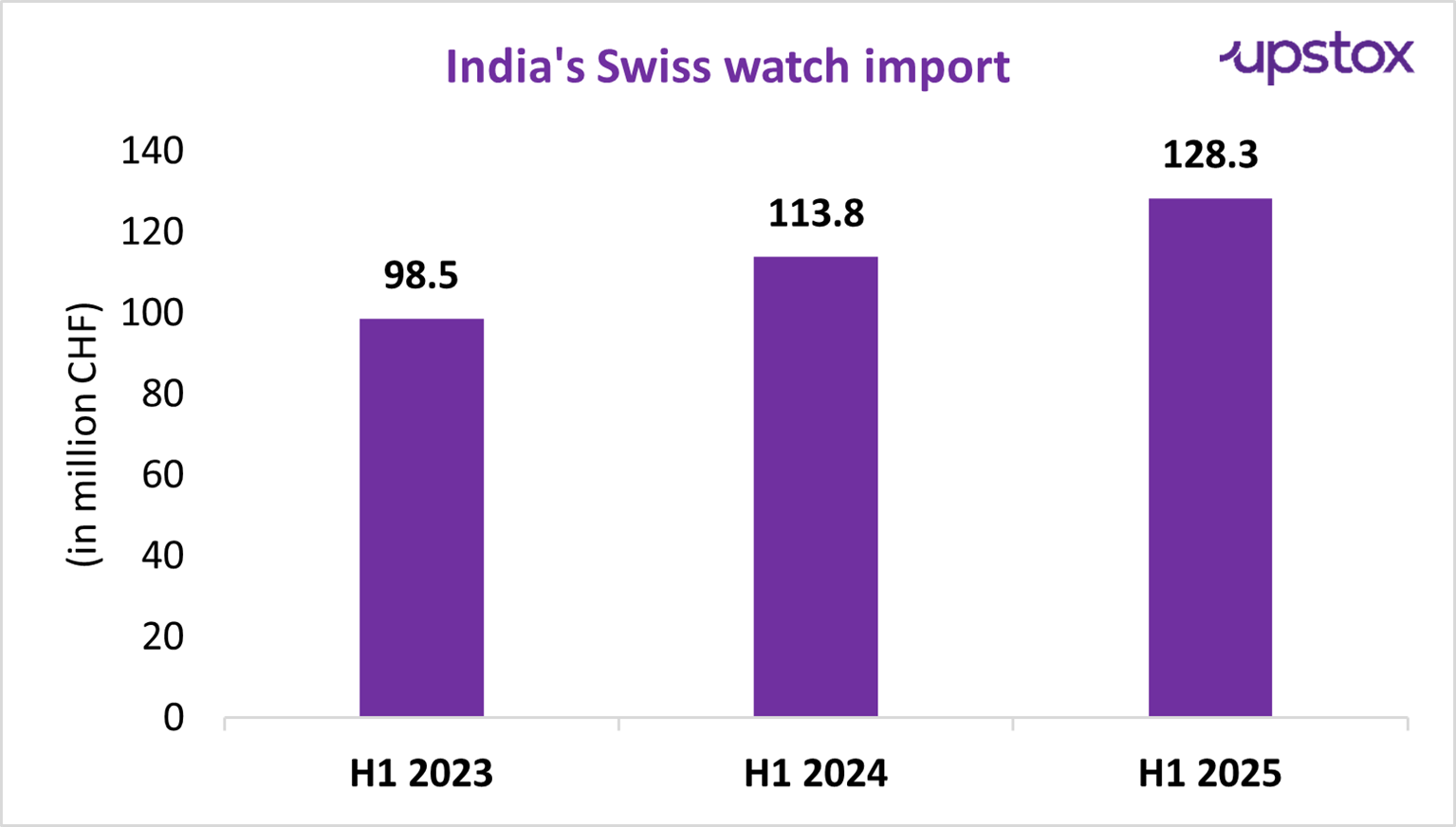

In 2024, Switzerland exported watches worth about CHF 274 million to India.

CHF is the Swiss franc, Switzerland’s currency, and that figure works out to roughly ₹3,151 crore at current exchange rates.

In a single year, Indians bought Swiss watches worth more than what many mid-sized Indian consumer brands generate in annual revenue.

The standout here is how quickly it grew. Swiss watch exports to India were over 25% higher than in 2023 and nearly 46% higher than in 2022.

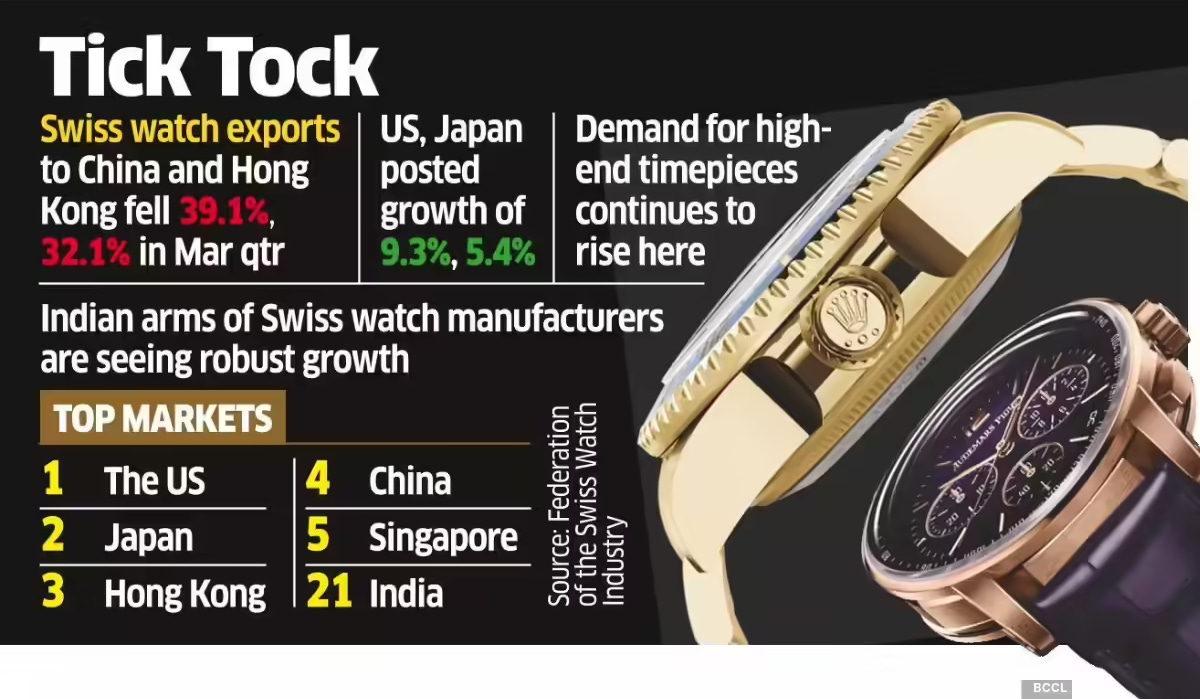

And this didn’t happen in a strong global year. The first half of 2024 was not a strong period for Swiss watch exports overall. Shipments to Asia fell by about 7.2%, dragged down by slowing demand in China. Years of property stress, weak consumer confidence, and tighter discretionary spending finally caught up with what had been the luxury industry’s most important market.

By early 2025, Swiss watch exports to China were down more than 13% year-on-year. Hong Kong followed a similar path. Japan and Singapore also lost ground.

India moved in the opposite direction. While much of Asia cooled, Swiss watch exports to India rose 12.7% in 2024 and grew by another ~9% in early 2025. In a year when most markets were buying less, India kept buying more. For Swiss watchmakers, it felt less like a spike and more like a quiet handover.

This isn’t a post-Covid sugar rush either. Over the last nearly two decades, Swiss watch exports to India have grown at an average rate of around 11% annually.

You can see the same shift playing out inside the country. In FY20, luxury and high-end watches accounted for roughly 48% of India’s watch market by value. After Covid, years of steady growth compressed into a much steeper climb. By FY25, that share had jumped to about 70%. Over the same period, the average price of a luxury watch sold in India rose from around ₹84,000 to roughly ₹2.04 lakh.

By FY25, that share had climbed to about 70%. Over the same period, the average price of a luxury watch sold in India jumped from around ₹84,000 to roughly ₹2.04 lakh.

Put simply, the centre of gravity moved.

Buyers who once spent years oscillating between mid-range or fashion watches are now skipping steps. The move from a casual watch to a “proper” Swiss watch is happening faster than it used to, sometimes after a single strong year at work, a promotion, or one well-timed payout.

So why now? Why didn’t this happen a decade ago?

For a long time, buying a Swiss watch in India simply didn’t add up. Import duties and taxes routinely pushed prices 20–30% higher than what the same watch cost in places like Dubai or Singapore. Anyone who could afford it simply waited for an international trip. That gap is now closing.

Under the India–EFTA trade agreement, which includes Switzerland, import duties on Swiss watches are set to be phased down to 0% over seven years.

For context: Historically, India’s luxury market was weighed down by high tariffs and slow, expensive market access. The agreement makes it easier for Swiss brands to operate locally, lower costs, and shorten the time it takes for new models to reach Indian shelves.

As duties come down and logistics improve, industry estimates suggest retail prices could soften by around 10–15% over time. And right now, India has far more people who can afford to care deeply about what they wear on their wrist.

India’s high-net-worth population has expanded sharply over the past few years. Estimates suggest the number of HNIs has grown by nearly 90% in roughly four years, driven by startup wealth, senior corporate compensation, professional services, and second-generation entrepreneurs scaling family businesses.

Many of these buyers see watches not just as luxury objects, but as passion purchases that sit somewhere between identity and asset. Even during periods of global uncertainty, this cohort hasn’t pulled back. The instinct is to upgrade.

Layered onto this is the rise of the HENRY demographic, high earners who aren’t rich yet, but are well on their way. These are professionals in their late twenties and thirties who prioritise quality, durability, and brand legacy over flash.

HENRY acronym: High Earner, Not Rich Yet

Together, these groups form the emotional backbone of India’s watch obsession. They want to own a luxury watch, understand it, justify it, and feel confident about the choice years later.

At the same time, the real momentum in luxury consumption isn’t coming only from ultra-rich families. It’s also coming from people who didn’t grow up around luxury but have grown into it quickly.

Doctors in their early thirties. Startup employees who benefited from one well-timed ESOP cycle. Lawyers, consultants, product managers, founders. People whose incomes jumped faster than their lifestyles did.

Multiple industry studies, including Deloitte’s luxury and consumer insights, point in the same direction: younger buyers are pushing India’s premiumization wave.

Around 60–65% of Gen Z and millennials say they want to buy more luxury items than previous generations, and are shifting their preferences from entry-level branded products to higher-end, more premium ones. Moreover, nearly 30% of them are comfortable spending more than ₹1.2 lakh on a single purchase.

Watches occupy a very specific psychological space for this group. You can’t wear your stock portfolio to a meeting. You can’t casually bring up your startup’s valuation at a family gathering. But you can wear a watch. In Indian social settings, that makes watches an efficient form of signalling. They communicate taste, success, patience, and insider awareness without demanding attention.

In fact, watches are increasingly viewed as visible wealth. A Rolex can take up to 500 hours to manufacture, and some models come with waitlists stretching six years or more. That level of production discipline shapes how people think about value. The watch doesn’t just feel expensive. It feels finite.

Some high-net-worth Indians now treat luxury watches as a small but deliberate part of diversified portfolios. Financial modelling suggests that portfolios with a modest allocation to watches, say around 10-30%, tend to show lower volatility and better risk-adjusted returns compared to traditional mixes of equities, bonds, and gold, even if returns are marginally lower.

Watches behave differently during market stress. During periods like the Covid-era volatility, their prices showed weak correlation with equity markets, making them feel less like a gamble and more like a stabiliser.

Scarcity pours fuel on this fire. Rolex is the best example. The most in-demand Rolex models in India today are the steel Daytona, the GMT, and the Submariner. Waiting periods can stretch into years. Allocations are limited.

When something remains hard to buy even after affordability stops being the constraint, it stops feeling like a product and starts feeling like a prize. Psychologists describe this as scarcity bias, reinforced by Veblen signalling, where limited availability increases perceived value.

At that point, buyers stop judging watches only by how they look or function. They start judging them by what they might hold onto over time.

And once that belief takes root, resale becomes inevitable.

In India, the pre-owned luxury watch market grew because people wanted access. Certified resale offers a way around multi-year waitlists, access to discontinued models, and reassurance that value won’t evaporate after purchase.

Industry estimates value India’s pre-owned luxury watch market at around $860 million, or roughly ₹7,903 crore (as of 23rd Jan, 2026), by 2030 , growing at over 11% annually. More than 50% of Indian luxury watch buyers say they’re open to buying pre-owned pieces, compared to a global average closer to 38%.

Why?

Because pre-owned solves three Indian problems at once.

Reduces entry cost.

Bypasses waitlists.

When done through authorised platforms, it removes the fear of fakes.

Brands have been forced to respond to this shift. Rolex, for instance, rolled out its Certified Pre-Owned programme globally after realising that the resale market had grown too large to sit outside the brand’s control. In India, authorised retailers have followed suit by setting up certified resale arms that offer authentication, warranties, and transparent pricing.

What surprises most first-time buyers is how prices behave in this market. Yes, in many cases, a watch bought second-hand can cost more than the official retail price. A Rolex that carries a retail price of around ₹15 lakh can sell for ₹30–40 lakh in the secondary market, depending on the model, availability, and condition.

This happens because retail prices are controlled, but supply is not. Brands intentionally produce far fewer watches than demand would justify. When demand consistently exceeds supply, resale prices stop reflecting age and start reflecting access.

Over time, this has created a clear hierarchy of value retention. Watches from Rolex, Patek Philippe, Audemars Piguet, and Omega are widely considered the safest bets in the luxury watch world.

In India, Rolex dominates this conversation because of its global recognition and consistency. Stainless-steel Rolex models, in particular, have never meaningfully depreciated since the 1970s, and some have fetched up to 200% of their original retail price in the secondary market.

Viewed structurally, the market stacks into layers. At the top sit aspiration-heavy brands like Rolex, Patek Philippe, and Audemars Piguet. Below that is the premium core, led by Cartier, Omega, Panerai, and IWC, typically priced between ₹4–10 lakh. Then comes the volume premium layer, anchored by Rado, Longines, TAG Heuer, and Tudor, followed by entry luxury brands like Tissot and Seiko.

At large Indian retailers, the top five brands account for ~65–70% of sales by value. India may enjoy browsing, but when serious money is spent, trust clusters around a narrow group of names.

Behind the counters, the business itself runs on tight economics. Gross margins for authorised retailers hover around ~20%, compared to 30–35% in Europe and the US. Discounting ranges from zero on high-demand models to 15–20% on slower-moving inventory, with most pricing falling somewhere in between.

Timing plays a bigger role in this business than most buyers realise. Nearly 60% of annual watch sales in India happen between September and March, driven by festivals like Diwali, wedding season, winter travel, and year-end bonuses. The rest of the year is quieter, which means retailers have to make most of their money in a fairly short window.

Looking ahead, the market doesn’t look exhausted. The pre-owned segment will likely absorb pressure from scarcity, becoming more organised and transparent as demand grows. Luxury watches in India are no longer occasional gifts, instead they are considered purchases, researched, debated, and planned.

For a country that once parked wealth almost exclusively in gold, that’s a meaningful change. Steel, ceramic, and sapphire crystal are now part of that mental map, not because they shine brighter, but because they carry stories, scarcity, and staying power. And that signals something bigger than watches. It shows how Indians are learning to think about value, identity, and long-term ownership, one deliberate tick at a time.

If you’ve made it this far, thanks for reading. We’ll be back next week, like clockwork.

Got a company, sector, or story you think we should dig into? Hit reply and tell us.

If we pick your suggestion, we’ll send some Filter Coffee merch your way.

Coffee Crew out.

Niceee

I THINK YOU GUYS SHOULD COVER SHOE INDUSTRY AND INDIAN METRO BRANDS LTD